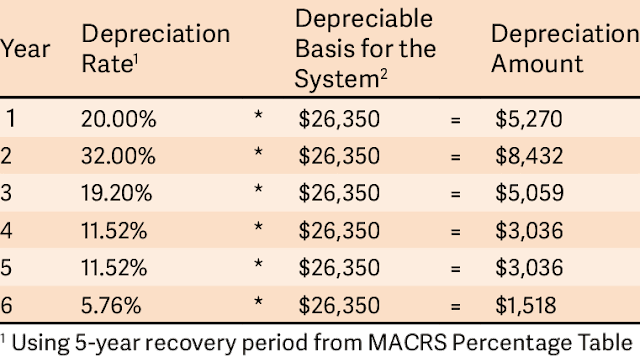

DEPRECIATION

|

| DEPRECIATION |

ពន្ធ គឺជាប្រព័ន្ធរដ្ឋបាលមួយដែលយកប្រាក់ពីប្រជាជន និងចំណាយទៅវិញដូចជាការអប់រំ សុខភាព និងសន្តិសុខជាតិ។ Taxation is the system by which a government takes money from people and spends it on things such as education, health, and defense.

|

| ឥណពន្ធ មានកន្លែងផ្ទុយគ្នាពី ឥណទាន Debits # Credits (Position) |

|

| ចំនួនទឹកប្រាក់ឥណពន្ធស្មើរនឹងឥណទាន Debits = Credits (Amounts) |

|

ប្រព័ន្ធឥណពន្ធ និងឥណទាន |

|

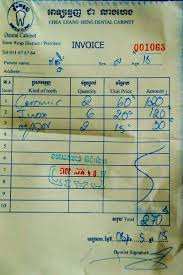

| Normal Invoice |

|

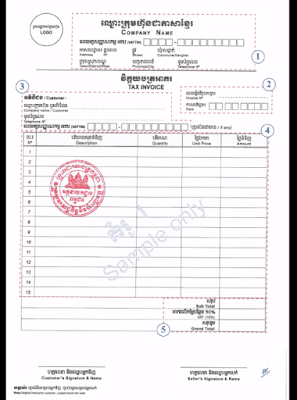

| Ex. Tax Invoice |

|

| Sample Tax Invoice |

|

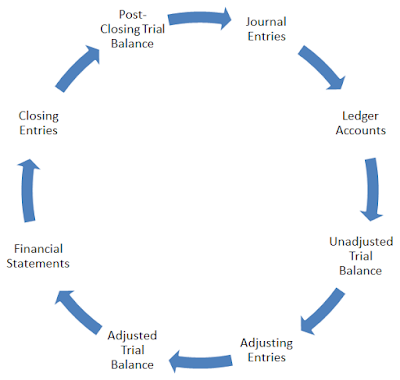

| Accounting Cycle |